Media Summary: In this session , we started by doing a brief test on country risk premiums. After a brief foray into lambda, a more composite way of ... Contrasts different approaches for estimating equity risk premiums in mature markets and extends these approaches to emerging ... In this session, we complete the discussion of equity risk premiums and start on measures of relative risk, arguing that while beta ...

Damodaran Implied Erp - Detailed Analysis & Overview

In this session , we started by doing a brief test on country risk premiums. After a brief foray into lambda, a more composite way of ... Contrasts different approaches for estimating equity risk premiums in mature markets and extends these approaches to emerging ... In this session, we complete the discussion of equity risk premiums and start on measures of relative risk, arguing that while beta ... In this session, we started by doing a brief test on risk premiums. After a brief foray into lambda, a more composite way of ... I am sorry but I had to reload this file. The previous one had issues with the slides) In this session, we started by doing a brief test ... In today's class, we started by looking how to measure a company's

Assess the historical and survey estimates of equity risk premiums as predictors of the future risk premium. In this session, we started by doing a brief test on the relationship between prices and risk premiums. We spent the rest of the ... In this session , we started by doing a brief test on the relationship between prices and risk premiums. We spent the rest of the ... In this session, I look at the process of estimating equity risk premiums, starting with the standard practice of looking at historical ... Implied equity premium: Finally, we computed an I had posted the video for this session a day ago (Sept 21) but the audio was missing from the last 20 minutes. Since I could not ...

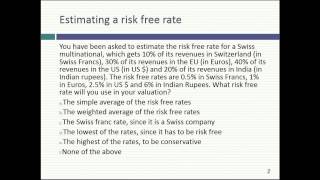

We started this class by tying up the last loose ends with risk free rates: how to estimate the risk free rate in a currency where there ... After briefly reviewing the weaknesses of historical premiums, we computed an