Media Summary: Financial Theory (ECON 251) Where can you find the market rates of interest (or equivalently the zero coupon bond prices) for ... Episode 10 of Algorithmic Trading 101 turns the duration and convexity primitives from the previous episode into actual trades. Cody Hyndman, Concordia University September 29th, 2021 Quantitative Finance Seminar ...

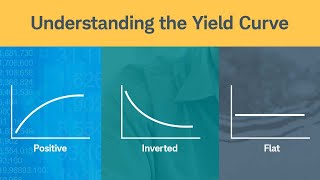

9 Yield Curve Arbitrage - Detailed Analysis & Overview

Financial Theory (ECON 251) Where can you find the market rates of interest (or equivalently the zero coupon bond prices) for ... Episode 10 of Algorithmic Trading 101 turns the duration and convexity primitives from the previous episode into actual trades. Cody Hyndman, Concordia University September 29th, 2021 Quantitative Finance Seminar ... A 15 minutes video with full of information about----- What Is a Subscribe to the Financial Times on YouTube: The difference between short and long-dated Treasury ... Break into finance today with out Financial Modeling Certification. Learn more at ...

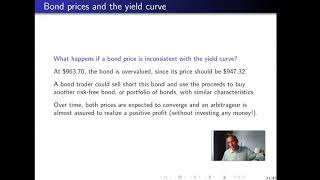

Introduction to the NOB (note over bond) spread using /S10Y and /S30Y futures products from the Smalls Exchange on the ... If you've been following what the Federal Reserve is doing with the interest rate, you have probably heard them talk about the ... FT markets reporter Colby Smith on the difference between three-month and 10-year Treasury ... between the two and ten-year Treasury notes the influencing factor for a Treasury spread trade is the